Accurate financial records stand as the backbone of any business. We’re talking about records that provide a rock-solid foundation, capturing exact figures about income, expenses, liabilities, and assets. These records act like a financial GPS, guiding businesses through both smooth and rough waters.

So, what makes these records accurate? It’s basically about consistency and precision. An accurate financial record will align with every penny in the bank account, every invoice sent, and every expense recorded. It’s about balancing the books with integrity, ensuring that everything matches up with reality.

Now, imagine a scenario where records aren’t up to scratch. It’s like throwing a wrench into the business machine. You can’t make informed decisions if your financial snapshot’s blurry. Inaccurate records can lead to misguided strategies, tax issues, or even legal troubles.

Let’s take an example. Suppose a small business fails to record all its sales. Not only do they miscalculate their profitability, but they also end up underreporting taxes. On the flip side, companies that prioritize accuracy can leverage their financial info to spot growth opportunities, cost-cutting options, and more.

We can all agree that numbers can either make or break your business. That’s why getting those digits in line and accurate is your best bet for financial health and peace of mind.

Strategies for Maintaining Accurate Financial Records

Keeping financial records accurate isn’t just about doing math. It’s all about developing good habits and using the right tools. Consistency is key here. Whether you’re jotting figures into ledger books or plugging them into software, accuracy starts with regular record-keeping practices.

Begin with collecting and organizing receipts, invoices, and bank statements and recording them promptly. It reduces the chances of forgetting transactions or losing important documents. Setting aside time each week to review and update records can really help in staying on track.

Taking advantage of technology is another big win. Accounting software can automate and streamline record-keeping tasks, making it much easier to avoid human errors while saving time. These tools offer features like automatic reconciliations and generate reports that keep everything transparent and clear at a glance.

Regular checks and audits are like a checkpoint for your financial setup. Scheduling periodic audits—internally or with a professional accountant—can provide insights into whether the financial records truly align with the business’s financial situation.

Beyond technology and practices, creating a culture of precision and accountability in your team makes a huge difference. Training employees on the importance of accurate record-keeping and maintaining an ethical mindset is pivotal in avoiding slip-ups and discrepancies.

Embracing these strategies doesn’t just save headaches down the line; it builds a trustworthy financial system that supports business growth and stability.

Steps to Recording Financial Transactions

Think of recording financial transactions as building blocks for a solid financial structure. Every entry you make contributes to the bigger picture.

Start with gathering all pertinent information on the transaction. This might include invoices for sales, receipts for purchases, and any contracts or agreements that authenticate the transaction. Having complete data on hand makes recording more efficient and accurate.

Once the information is ready, it’s time to dive into the accounting system or ledger. Enter the details meticulously, specifying the date, amount, account affected, and a brief narrative or note about the transaction. This will help in understanding the context when revisiting records down the line.

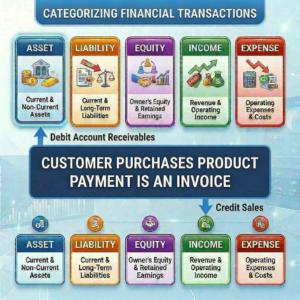

Categorizing each transaction properly is crucial. Assign transactions to the correct accounts—like assets, liabilities, income, or expenses—to provide a clear financial picture. Misclassification can throw off reports and lead to confusion.

Double-checking entries might seem a bit tedious, but it’s a step that prevents larger headaches. Reviewing entries for typos or mistakes ensures that the records remain precise.

The goal here is to keep records neat and tidy, like a well-organized toolbox. Accurate entry now saves a lot of trouble later, providing clarity and confidence that the numbers truly reflect the business’s financial activities.

The Significance of Accurate Financial Recordkeeping

Accurate financial recordkeeping is more than just a bookkeeping necessity—it’s a strategic advantage. The benefits extend far beyond merely having numbers on a spreadsheet.

When records are spot-on, businesses gain an insightful understanding of their financial health. It becomes easier to analyze profit margins, cost efficiency, and investment gains. This kind of clarity is crucial, especially when planning for future growth or tackling potential challenges.

Accurate records also play a critical role in compliance and tax reporting. Ensuring every transaction is accurately captured ensures that businesses align with tax laws and regulatory requirements. This minimizes the risk of penalties and audits, keeping the business’s reputation intact.

But there’s an even bigger picture here. Consistent accuracy builds trust with stakeholders, including investors, creditors, and partners. When they see well-maintained financials, it instills confidence that the business is managed with care and attention to detail.

Beyond the internal benefits, accurate financial records support external communications. They equip business leaders with concrete data to leverage when communicating with the media, discussing financing options with banks, or negotiating with suppliers.

In essence, precise recordkeeping acts as the fleet-footed compass guiding businesses through both calm and stormy times. It’s reassurance that the ship is steady and on the right course.

Challenges and Solutions in Accurate Recordkeeping

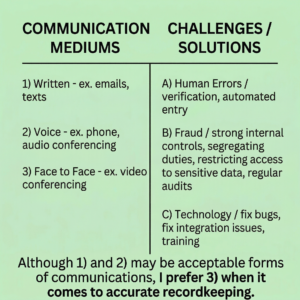

Navigating the world of financial records isn’t without its bumps, but acknowledging potential challenges upfront can help you tackle them head-on. One common hurdle is the potential for human errors. Whether it’s transposing numbers or misfiling receipts, mistakes happen. The solution lies in deploying double checks and utilizing technology to minimize manual entry where possible.

Fraud presents another significant challenge. Safeguarding against fraudulent activities involves implementing strong internal controls. Segregating duties, restricting access to sensitive data, and regular audits can help spot unusual activity early.

Technology offers great aid, but it’s not foolproof. Software systems sometimes face integration issues or technical glitches. Keeping tech systems updated and ensuring they are well-integrated can circumvent many of these issues. Also, training is key. Investing in training sessions for all employees involved in handling financial data keeps everyone on the same page.  It’s crucial to keep the workforce informed about best practices and evolving tools.

It’s crucial to keep the workforce informed about best practices and evolving tools.

To top it off, building a culture where accuracy is prioritized creates a team more mindful of their primary tasks. Encouraging open communication about challenges helps in finding timely solutions and keeps the recordkeeping process as smooth as possible.

Addressing these challenges proactively ensures that businesses not only maintain precise records but also build a resilient financial architecture that supports overall growth.